Regional bank dealmaking heated up considerably in the second half of 2025. Comptroller Gould’s comments on the removal of artificial bank size regulatory heightened standards blew significant winds into regional banks’ sails, yielding, a wave of activity in that space that has not been present for many years. Scale, geographic diversification, and physical presence in attractive markets were the drivers of this large bank mergers. The regulatory step-back allowed market forces to prevail, and, with them, unleashed M&A activity of larger banks, some of which are motivated by catching up to the top five.

M&A can be an effective response to the need to deploy new, often scale-intensive technologies leading to greater efficiency. While the largest transactions get the most ink, there is much activity among smaller institutions facing the same challenges at all levels, from banks under $1B in assets to much larger ones. The changing regulatory posture toward bank M&A pours additional fuel to the transaction stream and helps close proposed transactions at record speeds. We have all been scarred by deals that got held up in regulatory purgatory for a year or more, some to be rejected after two years of review. It appears that those are firmly in the past.

Another new trends is the involvement of non-bank in M&A. Private Equity firms started rolling up wealth companies and IRAs in recent years, raising the prices for such potential acquisition targets for all players. Payments and fintech organizations are now considering similar deals to drive growth and scale as well as purchase funding bases they cannot de novo themselves. Larger banks are also on the hunt for payments companies that will enrich their current offerings and improve their fee income performance.

This year’s resurgent IPO market for fintechs could be a leading indicator that the industry will find ways to engage in AI powered products and payment capabilities. So far this year, six US fintech IPOs raised about $3.2 billion, the highest level in at least a decade, according to S&P Global Market Intelligence data. Timing is good for M&A for other reasons as well. Banking fundamentals are healthy with earnings boosted by growing net-interest margins while loan provisions remain stable. The concept of digital transformation has matured into “Synergies plus transformation” which many consultants consider essential I, a nay sayer, consider this an elusive goal that requires much more than a prudent acquisition strategy. Cost reduction levers (rationalizing branches, reducing overhead) are just one aspect of a deal’s thesis. Now, value theoretically comes from tech simplification and core modernization along with greater efficiency. Unfortunately, many such promises have not come to fruition.

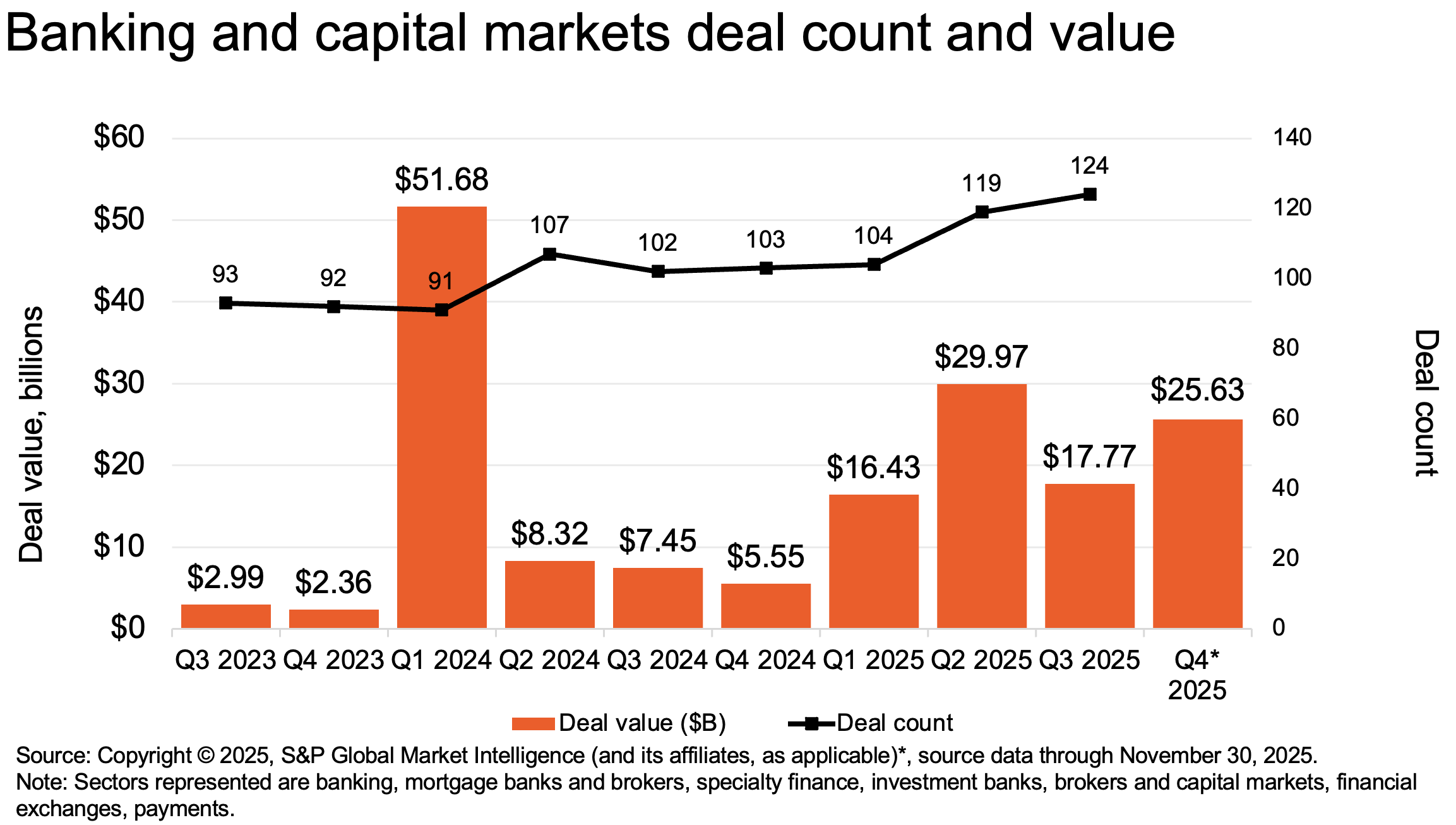

15.4% of banking and capital markets deals this year are worth $500M or more, the highest since 2021

As mentioned, the competition for M&A targets is intensifying as we speak. Not only are traditional bank players looking for growth via acquisition, but non-banks are in the market as well, and their financial situation is often superior to the banks’ given their regulatory structure. Acquiring banks must also be mindful of the post-acquisition balance between fee income and interest income, plus the franchise value implications of the resultant combination.

Regulatory easing and repositioning, declining interest rates and strong credit metrics are all fueling the next M&A wave. Social issues, while eternal, are less of a hinderance considering the vital importance of stable funding sources, growth and efficiency moves. And yet, we’ve seen massive value destruction as deals do not materialize as envisioned. Execution risk is, in my mind, the highest risk associated with M&A, matched only by falling in love with a deal and overpaying for it. So, while the opportunity is ripe, the risks aren’t diminished. Building benchmark discipline around acquisition pricing and integration will increase the likelihood that your next transaction fulfills and possibly exceed expectations.